PAXAFE just wrapped up another LogiPharma conference just three years after attending our first ever conference!

Ahh to go back to the days when we were the sole, shiny new booth in the room championing the importance of context, data actionability, agnostic visibility, transportation performance and risk!

Now it’s risk this and decision support that, and AI this and that — making the parsing of substance vs. noise tougher.

This year, we did something different: we did ZERO pitching. Zip.

Not until we understood WHO you are, WHAT problem you’re trying to solve, and WHY you NEED to solve it NOW.

What we did instead was engage in real-time discovery and have real, genuine conversations surrounding pressing issues and problems to understand whether PAXAFE was best suited to help.

If we are, we’ll say so.

If we’re not, we have a network of great partners whom we’ll happily refer.

The results? Shocker — people are more than willing to share their list of problems if they think that you can help.

And as such, from relationships crafted at our booth, our dinners, our presentations, our tiny meeting pod — we’ve walked away with a refreshed perspective on Pharma / Life Sciences transportation and logistics needs, where we can help, and where we can be a conduit.

This year, I’m going to take a different approach to my annual list of takeaways.

First, I’m going to grade myself on the last list that I created 6 months back — what I got right, what I got wrong, and what has yet to play out.

Only then, will I add additional takeaways that are net new to the list.

But first, a reminder: who is PAXAFE?

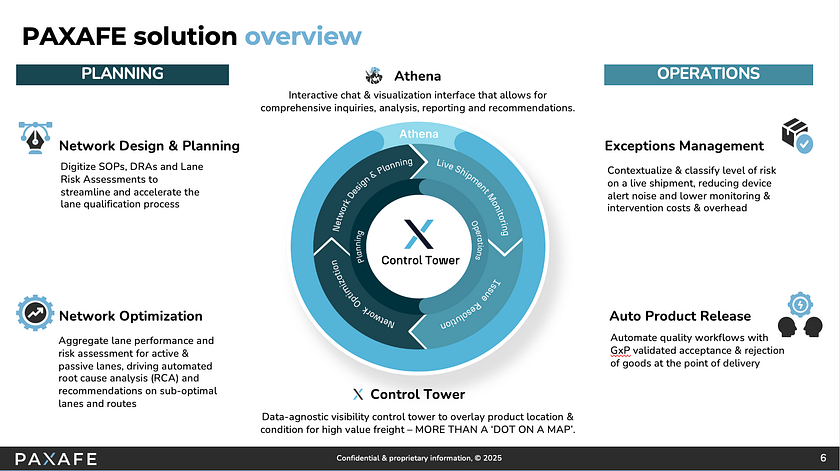

PAXAFE is a logistics orchestration & decision intelligence platform for cold chain & valuables.

At the core is its data-agnostic visibility control tower that overlays active & passive device data, carrier milestones, ELDs, and any other relevant transportation data in a single map view and tied to the same shipment / load.

This data overlay is critical — first, it supplements missing or less than ideal data. Second, it helps your team gain confidence in the source of truth data towards both location and temperature.

PAXAFE’s control tower is surrounded by an intelligence layer, which is broken out into 2 categories: operations vs. planning:

Operations (means pressing action necessary on live shipments to improve performance, reduce risk or close out a shipment):

- Live shipment exceptions management to reduce hyper-care monitoring costs

- GxP validated automated product release & stability budget

Planning (means aggregated intelligence to be used towards future shipments):

- Lane Qualification: Digitized SOPs and risk assessments with accurate risk scoring

- Lane Performance & Risk Monitoring: Lane, route & shipment performance & risk, with prescriptive, hyper-contextual recommendations across problematic lanes & routes in accordance with SOPs and existing processes / workflows

Each critical functionality is overlayed with AI to accelerate workflows and time to make faster, better decisions

Let’s start with last year’s list!

ONE: IoT adoption is quick, but rollouts are slow

Ok, that’s kind of an oxymoron — I get it.

Pharma companies are making swift decisions around justifying the value of IoT and visibility and deciding to move forward with deployment.

That being said, when it comes time to actually deploy the devices, there are all sorts of roadblocks:

- Change management: there’s buy-in at a corporate level or at a senior level, but regional leaders / operations are not empowered or incentivized to ensure local success of rollout

- Device issues: devices are on their best behavior during the validation phase, but once you start scaling to thousands of devices, ping rate consistency, signal strength and battery reliability become problems

- Lack of KPIs or objectives in knowing what visibility will be solving for. It doesn’t always have to be that IoT needs to solve for product loss. Sometimes, it’s solely about having the data to make quicker, smarter network decisions for the future, and that’s OK.

2025 follow up:

This is still undoubtedly true. The device players that have been around for a while are elevating their performance, but change management and centralized program KPIs continue to be under-focused.

Pharma continues to be bullish on IoT implementation, especially with how much innovation we are seeing from the device providers.

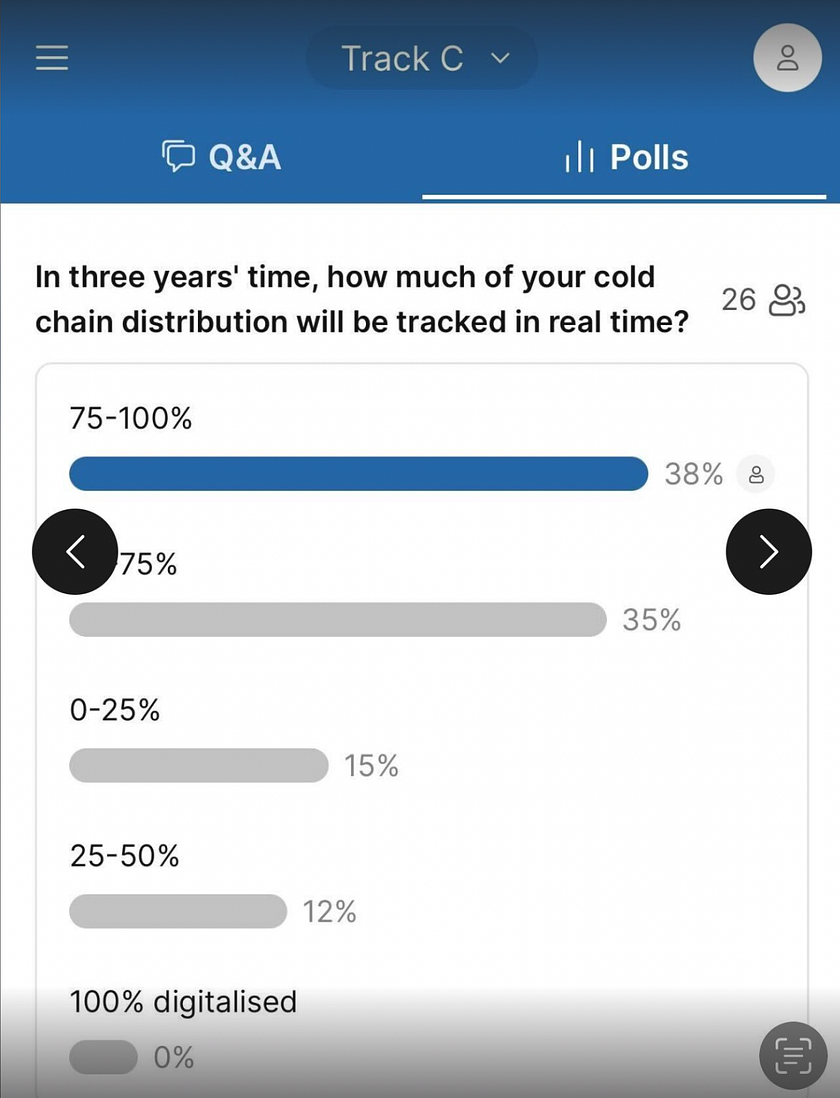

73% of respondents (room full of Pharma executives) had indicated that they expect between 50%–100% of their cold chain distribution is expected to be tracked in real-time within 3 years.

Recent examples include Sensitech’s new GEO-X tracker, Tive’s new pharma tracker, and Frigga’s recent announcement of a partnership with SkyCell.

We’re actually seeing a bit more differentiation in hardware than I thought there would be a few years back — from how you build the screen and which temperature parameters it can endure, button vs. no button, reverse logistics strategy, monitoring service vs. no monitoring service, data differentiation (e.g. focus on ports and airport gateways vs. all the way through), probe vs. no probe (and does it actually work), etc.

This means that Pharma’s control towers must be able to look dynamically at sensor performance across region, mode of transport, manufacturer, positioning / SOP, etc. and manage proactively.

TWO: There are still two different schools of thought in terms of consolidation vs. separation of powers

Some pharmaceutical companies prefer to procure agnostic capabilities through channel partners that they’re already working with. This drives consolidation of vendor base and provides ‘one less partner’ to manage / work with.

Others want to have a complete separation of powers so that they’re not tethered to any one service provider — whether it be a 3PL, and IoT device provider or a packaging provider.

Both options come with their pros and cons.

2025 follow up:

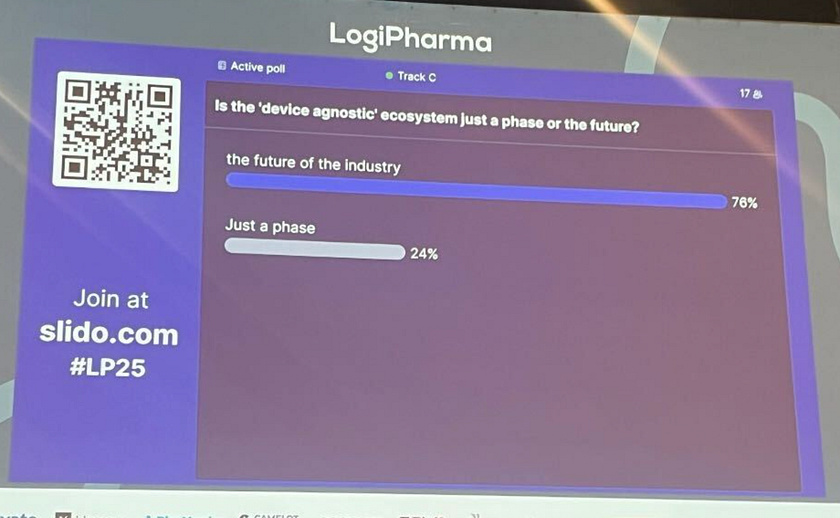

OK — there has been a material swing towards the agnostic control tower pathway, and it feels like it has just happened in the last 12–18 months.

I believe this was brought about by 3 reasons:

- Pharma originally thought that it would ‘marry’ and partner with 1 or 2 device providers forever. Or at least a really long time. And that it would make sense to use their control tower. Except when device issues, battery issues, calibration, capacity, difference in source of truth transportation data — you name it — happens, they realize that a parallel device sourcing strategy is a must. A parallel device sourcing strategy would require multiple control towers, and would be riddle with conflict of interest.

- Device innovation pace: Hardware providers have started investing in edge, and improvements to their hardware / firmware / software is happening more rapidly than anticipated — which lends a case towards playing nice with everyone, and using the right partner for the right use case as improvements are made.

- Poor functionality: Hardware companies are not software companies. Their limitations around building a world-class control tower and AI-enabled solutions pushes Pharma to explore ancillary products, which prevents them from consolidating everything ‘under one roof.’ The end result could look like 2 or 3 different platforms for active IoT, 1 or 2 different logins for passive data, 1 or 2 different logins for carrier milestones, 2 or 3 different logins and systems for SOP & quality management, and at least 1 login for advanced, aggregate analytics. That’s a headache!

3 out of 4 Pharmaceutical executives believe that data agnostic platforms are the future.

The market agrees that consolidation of capabilities that are not tethered to one device, packager or LSP is the trajectory we are now on.

THREE: Visibility Objectives are Fragmented

We spoke to a Pharma leader that told us that he doesn’t really care about saving ‘onesie twosie’ shipments — he cares about what actions he can take to prevent future losses en masse. Or reducing CO2 footprint. Or optimizing packaging performance. Or having the confidence to convert Air shipments to Ocean shipments.

We spoke to another Pharma leader that, upon seeing PAXAFE’s dynamic Lane Risk Assessment (LRA) tool (which helps do all of those aforementioned things!), said — “yeah, but how’s that going to help me intervene with problematic live shipments?”

These two individuals were from the same company.

We’re finding that functionally speaking, Quality, Transportation / Logistics and Supply Chain Planning care about fundamentally different things. And there’s a good chance that they have limited interaction with each other internally.

Secondarily, we’re also finding that more senior leaders are caring more and more about big ticket savings opportunities (forward looking), while mid-level leaders are more prone to focus on the here and now (live shipments).

And if you ask 3 different people from the same company as to why their company is investing in Visibility, it’s likely that you’ll get 3 different answers.

2025 follow up:

This is still painfully true.

Perhaps there has been some re-emergence of common ground towards macro factors (e.g. how tariffs and potential re-shoring impact the supply chain, flexing away form China (e.g. India) and what that supply chain would look like, etc.

But generally speaking, different functions want different things.

Some people purely care about salvaging an at-risk shipment, and don’t care about planning optimization one iota.

And vice versa.

PAXAFE has found that the most effective way to drive alignment is to mandate a steering committee, with leadership and execution teams that are driving decisions across quality, transportation, planning and … FINANCE!

Yes, finance. If you want to recognize savings, they need to be bought in and on board.

FOUR: Renewed Interest to Digitize Passive Data

For decades, temperature data loggers were the unsung heroes for quality leaders trying to determine whether a product should be accepted, rejected or quarantined.

Once real-time IoT sensors are fully vetted and their platforms are GxP validated, passive loggers are no longer needed.

That being said, the slow rollout and constant hurdles of IoT deployments (mentioned in point 1) is giving reason for Pharma to continue investing in Passive data.

Today’s problem with passive data lies in:

- No centralized repository for all passive data, with different Pharma regions having different SOPs around passive data collection & retention

- Manual product release process (for product approval, rejection)

- No passive lane insights at scale — limited understanding towards the performance of passive lanes

- Expensive middleware from sensor providers that are specific to one provider — making it more challenging and expensive for Pharma companies using 2 or 3 manufacturers

Pharma is coming to the conclusion that the majority of their lanes are still passive, and that they can make use of all of this data to establish some performance baselines, using it as a stepping stone to understand which lanes to prioritize with real-time IoT deployments.

2025 follow up:

Ok — 100% yes. But not for the reason I had originally expected.

Years ago, when PAXAFE started ingesting and displaying passive data, I thought it was because Pharma wants to leverage insights to improve passive shipping lanes.

Nope. Well, partially.

First, they want to overlay passive temperature data with carrier milestones to yes — get better context around lane performance on their passive lanes.

BUT MORE IMPORTANTLY: They want to overlay passive temperature data with active IoT temperature data to qualify their IoT devices, get confidence in their temperature accuracy, and eventually remove or minimize the number of passive loggers used in the network.

FIVE: There’s an Opportunity to Improve the TRUST LAYER between Pharma and IoT

Pharma is placing some of the blame on delayed IoT rollouts attributed to lackluster device performance and device challenges, and then poor intervention services when temperature excursions get missed / are not actionable.

On the flip side, device providers are attributing many of the challenges towards over-promised demand and poor change management.

The reality is that there’s a little of both at play, and there’s an opportunity to build trust through flawless execution.

This means device providers have to be transparent and proactive when their devices are malfunctioning. And Pharma companies must adhere to financial commits and projections associated with inventory deployment.

2025 follow up:

Generally speaking, the relationships between Pharma and device providers remain strong.

There is some sense of loyalty and kinship towards those providers that moved heaven and earth to help Pharma get through the pandemic.

However, the sentiment that IoT and visibility have not delivered on its promise of reducing product waste, optimizing transportation performance and enabling faster decision-making is absolutely there.

And Pharma is making practical decisions to make sure those deliverables are met, or else there is little point in spending millions annually on devices.

Six: 🤑 Monitoring is too Expensive 🤑

Monitoring service teams are charging Pharma anywhere from $10/shipment all the way up to $200+/shipment, depending on the level monitoring and intervention / action that is required.

This makes sense — having one person oversee the monitoring of hundreds of shipments per day… 15% of which will see some form of device alert and require some level of investigation… is not an insignificant task.

Pharma is seeking to understand how technology can augment productivity, and enable each monitoring agent to reduce device alert noise and only truly respond to alerts that pose a real risk to the product.

2025 follow up:

Monitoring is usually a painful conversation.

Spending $200-$300 per shipment in hyper-care costs, plus seeing product loss and inefficiency cuts twice.

At PAXAFE, we’ve come to the realization that device alerts are actually a poor proxy towards actual live shipment risk.

We’ve developed a series of algorithms that monitor holistic shipment risk, reduce the number of actual alerts that teams must respond to, and enable Pharma teams to lessen their reliability on hyper-care or mandate that their monitoring teams become more productive.

Pharmas’ focus to reduce monitoring spend is acute.

Seven: Logistics Service Providers (LSPs) are looking for ways to add more value and defend visibility’s ROI

There is still a race towards a cell-enabled hardware label that’s very much happening — the same race I’d mentioned back in 2022.

But until cost of components and hardware / firmware performance reach a state of feasibility, device providers are starting to look at other ways to add value.

This can include aggregate insights, packaging optimization consulting, custom reporting, monitoring & intervention services, etc.

As such, many of these LSPs are going through multiple decision points:

- Do we build versus buy?

- If we build, does that mean we need to materially change our hiring strategy?

- Do we verticalize for Pharma, who has unique requirements and workflows? Or do we implement something more generic for all of our customer segments?

- Are we going to cannibalize our existing services, or enhance them?

- Are we going to push towards more predictable software revenue, or find ways to charge transactionally?

That said, merely having a solution is one part of the equation. The more difficult part of the equation is aligning on the value quantification.

Pharma needs to have baseline data that already quantifies and establishes some of the following:

- full cost of a temperature excursion

- full cost of a delayed shipment

- time and cost associated with product release

- time and cost associated with validating a lane

- time and cost associated with packaging validation / simulation

- time and cost associated with IoT device validation / selection

- cost associated with route non-conformance

- inventory / turn cost associated with each incremental day that’s a part of a contracted lead time parameter

- time and cost associated with making a major Lane SOP parameter change (e.g. switching from air to ocean on a particular lane)

- Many others

In many cases, Pharma does not have this readily available — which makes value discussions more challenging for providers.

2025 follow up:

We believe that we’re also looking at some kind of inflection point here. Just at this conference and shortly before, PAXAFE has been re-engaged by several major LSPs that have at one point or another either decided to ‘build’ internally, or were undecided.

They have since returned and determined that they’re re-evaluating that strategy and are now more prone to buying.

A few reasons:

- Not their core focus — their core focus is providing their customers with the best transportation service in the movement of goods from point A to point Z

- The pace of innovation around areas like AI make it difficult to stay up to speed and on the cutting edge of what’s possible

- Expensive to build and maintain, with delayed time to value in market

- Pharma less likely to trust it unless there’s a ‘separation of powers’

Eight: GenAI Doubted, But Shows Promise When Backed By Evidence

We hear doubt around the promise of GenAI after someone goes into ChatGPT, uploads some data and asks a few questions like “where is my risk today?” or “show me my delayed shipments.”

LLMs have no inherent comprehension of risk, delayed shipments or what’s important to you within the context of your cold chain transportation network. It doesn’t know what’s ‘normal,’ what your SOPs are, how you address or react to risk, and so forth.

To truly understand what’s possible, companies need access to a tuned model that understand the intersections of risk, decision intelligence, custom workflows, transportation and cold chain requirements — that’s been built on an underlying risk management infrastructure.

They’ll also need access to A LOT of training data.

2025 follow up:

In 2025, Pharma is more bold and aggressive towards pursuing the incorporation of gen-AI.

1-year ago it was objection after objection — “I don’t believe it works,” or “does that mean ChatGPT gets access to my data?”

Today, some of those concerns linger, but there’s a realization that not moving forward is moving backwards. And nobody wants to get left behind.

So — how about some new findings in 2025?

ONE: Pharma is now more open to partner on quality decisions / product release with partners

When engaging with control towers, Pharma companies have a few choices with regards to product stability ranges, time out of range (TOR) and product release:

- the control tower can be a platform that provides intelligence and analytics, but most quality decisions are triple checked and completed manually as per SOP

- the control tower gets GxP validated, and goes through a validation exercise with said Pharma so that quality teams know that they can trust the data

Anecdotally, I would still put a majority into the manual bucket, but significantly higher numbers of Pharmaceutical partners are now considering (and going through the exercises) of validating external partners to drive product release decisions.

Two: From monitoring to decision intelligence — visibility KPIs are evolving to be more strategic

The common contention with visibility programs by some in the industry has been ‘well my network doesn’t have much product loss’ — or ‘my product loss only happens in the final mile.’

Sometimes that is accurate, and sometimes that’s based on anecdotes and perception, where we learn otherwise through the aggregation of historic data.

The broader point, is that the majority of savings are not going to come salvaging a few shipments per year. Don’t get me wrong — saving shipments isn’t just about product preservation, but it ties to patient health, customer happiness, product replacement, inventory strategy, root cause and corrective action procedures, etc.

Each ‘deviation’ that triggers a disposition process is actually quite expensive for pharma to manage through the QA process.

That said, Pharma now recognizes and seeks out opportunities through parameter optimization:

- Having the data & confidence to change mode of transport from air to ocean

- Having the data to drive packaging optimization— reduction of thermal life, active to passive, or shipping in 2–8 to 15–25 ranges (much cheaper), but taking additional precautions

- Optimizing routing & shipment SOPs to minimize inventory carrying costs and lead time with customer

Operationally, the monitoring focus has turned from ‘salvaging product’ to:

- Reducing monitoring costs and maximizing productivity

- Reducing hyper-care services

Three: Small and mid-sized Pharma getting involved earlier

Pharmas with just a product or two, and more on the way over coming years want to do the work now to get things right prior to hyper-scale.

Changing data infrastructure, endpoints, and control tower strategies is much more difficult as a $50B company vs. a $1B company.

Our team has embraced the opportunity and envision a world where every cold chain shipment is tracked, monitored, and analyzed for the greater good.

ABOUT PAXAFE:

PAXAFE is a logistics orchestration & decision intelligence platform that helps cold chain manufacturers and Logistics Service Providers (LSPs) reduce monitoring & intervention costs [for IoT-enabled visibility], digitize & automate Lane Validation and Lane Risk Assessments (LRA), and incorporate prescriptive recommendation into the real-time visibility network.

Acting as the trust layer for temperature-controlled logistics networks whose mission is to drive towards zero waste in cold chain transportation, PAXAFE is backed by VC / CVC investors like Microsoft, Northwestern Mutual, Framework Venture Partners, Ubiquity Ventures, Venture53 & the Founder / CEO of Project44.

If you want to learn more, please reach out to ilya@paxafe.com